7 Best Ways to Embed Revenue-Based Financing in SMB Software (2026 Guide)

The vast majority of vertical SaaS solutions hold several months worth of transaction data about SMBs (Small-Medium Businesses) that go entirely unused as a potential revenue stream. That same transactional data used to create your analytics dashboard (payment volume, revenue trends, invoice cycles, and refund patterns) is the data required by an embedded finance engine to approve a working capital offer in hours, rather than weeks.

Embedded revenue-based capital within SMB software is experiencing phenomenal growth. Based on recent research, global revenue-based capital is estimated to be worth $67.73 billion within the next 7 years (by 2029) at a CAGR of over 62%. Parafin has already approved more than $25 billion in capital offers through companies like Amazon, DoorDash, and many other vertical SaaS applications. For example, Shopify Capital funded more than $4.2 billion to its merchants as cash advances in 2026, compared to just over $3 billion the year prior. These companies are not lenders; they are software applications who realized that their transaction data is more useful as a form of collateral than an actual credit score.

Three key factors differentiate between the successful and unsuccessful embedded providers of revenue-based finance. They are:

1) The correct data architecture.

2) The correct infrastructure partner.

3) The correct rollout plan.

We provide a detailed overview of all 7 best practice approaches related to the following: 1) the selection of an infrastructure provider; 2) the development of an underwriting data layer; 3) the steps needed to integrate; and 4) the most common mistakes made during implementation.

What Is Revenue-Based Financing in SMB Software?

Revenue-based financing, often called RBF, is a capital model where a business receives an upfront lump sum in exchange for a fixed percentage of its future monthly revenue. Repayment continues until a predetermined total the principal plus a flat fee is paid back in full. Payments flex with revenue performance: higher during strong months, lower when sales slow down. There is no fixed due date, no equity dilution, and typically no personal guarantee required.

When embedded directly inside SMB software, RBF removes the need for a merchant to visit a separate lender or fill out a loan application. Instead, the platform that already processes their transactions whether that is a point-of-sale system, an e-commerce marketplace, or a vertical SaaS tool surfaces a pre-approved capital offer based on behavioral and revenue data it already holds in real time.

This is a fundamental shift from how small business lending has worked historically. Traditional banks rely on backward-looking credit scores and collateral. Embedded RBF platforms rely on live transaction signals which are both more accurate and far more accessible to the businesses that need capital most.

Technical Note: RBF differs from a Merchant Cash Advance primarily in repayment mechanics. MCAs typically use daily deductions tied to card batch settlements and carry higher factor rates. RBF uses monthly revenue percentages with a clearly defined repayment cap. For longer-term growth financing inside a software platform, RBF consistently produces better unit economics and lower default rates for both the merchant and the platform.

Why SMB Software Platforms Are the Ideal Channel for Embedded RBF

Here is the core problem that embedded revenue-based financing solves. Traditional banks take six to twelve weeks minimum to approve an SMB loan. According to Plaid’s analysis of the UK market, 57% of all SME credit applications are either abandoned because the process is too difficult or ultimately rejected outright. The bottleneck is not the availability of capital. It is data access and distribution speed.

Your vertical SaaS platform already solves both of those problems at the same time.

On the data side, you already process the merchant’s transactions, track their revenue trends, and in many cases connect directly to their accounting software. You have better underwriting data than most banks ever will. On the distribution side, your customers open your platform every single day to run their business. A pre-approved capital offer surfacing inside that workflow does not feel like an advertisement it feels like the platform serving them at the right moment.

Furthermore, the commercial upside for the platform is substantial. Research from Adyen found that platforms extending beyond payments to offer embedded financial products can increase revenue by three to four times through new subscription tiers and fee structures. That is the platform data flywheel in action: more financial products drive deeper customer integration, which improves retention, which generates more data, which enables better underwriting.

The SMB software market itself is valued at approximately $79.82 billion in 2026 and projected to reach $151.74 billion by 2035. Platforms that embed financial services today are building a structural moat inside that growth curve and the ones moving first in each vertical are capturing disproportionate share.

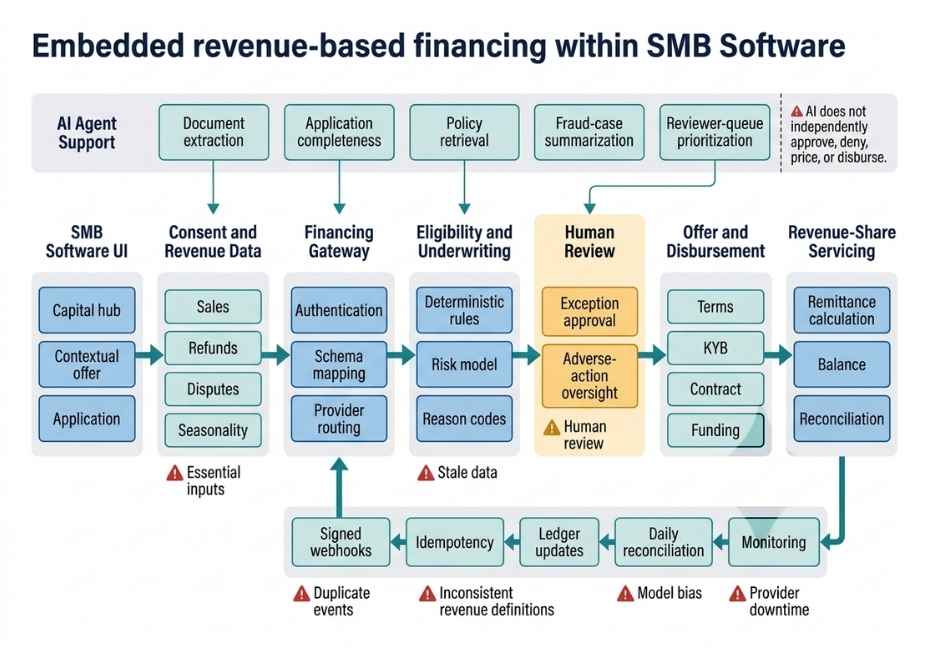

How Embedded RBF Actually Works: The Underwriting Data Architecture

The most important thing to understand is that the core of any embedded RBF product is not the loan itself. It is the underwriting data layer sitting underneath it. Platforms that win in embedded lending combine three data sources rather than relying on any single one.

Banking transaction data shows cash flow reality. It tracks what comes in, what goes out, overdraft patterns, and existing debt obligations. This data is pulled via open banking APIs such as Plaid or through CFPB Section 1033-compliant data feeds that give lenders credentialed access to bank account history.

Accounting records provide the financial narrative. Profit and loss statements, outstanding invoice aging, accounts receivable balances, and tax records are integrated through connectors to QuickBooks, Xero, or NetSuite. This layer catches discrepancies between what a merchant says and what their books actually show.

Commerce and platform activity is the most powerful layer of all and your platform already owns it natively. Real-time sales volume, refund rates, customer retention metrics, and seasonal patterns are signals that no external lender can access without your cooperation.

Did You Know? According to research cited by Luca AI, approval speed correlates directly with data integration depth. Platforms with direct API access to commerce, payment, and accounting systems approve SMB financing in hours. Those requiring manual financial statement uploads take weeks. Traditional banks take six to twelve weeks minimum.

When all three layers combine, the underwriting engine cross-references live transaction behavior against self-reported financials, significantly reducing both fraud and approval latency. This is the unified data layer architecture that powers the best-performing embedded lending programs in the market today.

The 7 Best Ways to Embed Revenue-Based Financing in SMB Software

1. Partner With an Embedded Lending Infrastructure Provider

The single fastest path to embedded RBF is integrating with a purpose-built infrastructure provider rather than attempting to build underwriting, compliance, and loan servicing in-house. These providers handle credit risk on their own balance sheet or through bank partnerships. Your platform earns a revenue share on every dollar of funded volume, with no credit exposure.

This model is sometimes called the embedded lending infrastructure model, and it has become the dominant approach for vertical SaaS companies in 2026. The reason is simple: the compliance burden alone state lending licenses, KYB and AML screening, CFPB open banking rules is genuinely complex. Infrastructure providers absorb that complexity entirely so your engineering team can focus on the user experience layer.

2. Here is how the leading providers compare:

Parafin is best for marketplaces and high-GMV vertical SaaS platforms. Its machine learning underwriting engine is trained on data from over two million small businesses. It powers Shopify Capital and has processed capital offers for DoorDash merchants, Amazon sellers, and dozens of other platforms.

Kanmon is best for vertical SaaS and B2B SaaS with SMB customer bases. It offers term loans, lines of credit, invoice financing, and accounts payable financing. Notably, Kanmon does not require a platform to offer embedded payments before adding lending though payment data improves underwriting accuracy when it is available.

Liberis is best for merchant-facing platforms with significant card processing volume. It offers white-labeled, revenue-based capital products with strong coverage in the EU and UK markets.

Pipe is best for SaaS platforms with predictable recurring subscription revenue. Its revenue advance product adjusts repayment to match your customers’ actual sales, not a fixed schedule.

Unit is best for mature platforms that want to build custom financial products. It offers a full banking-as-a-service stack that can be paired with custom RBF product configurations for more sophisticated implementations.

Pro Tip: Both Parafin and Kanmon allow platforms to surface financing offers without holding any credit risk themselves. The platform provides the data access and the in-product surface area. The infrastructure provider handles origination, underwriting decisions, compliance, and loan servicing entirely behind the scenes.

3. Start With Your Existing Payments Data Before Building External Integrations

A common mistake is waiting until all three data layers are integrated before launching. Do not do that. Start with the transaction data your platform already has, because that is enough to begin.

A platform processing between $50,000 and $500,000 per month in SMB payments already has the core underwriting signal needed to generate pre-approved working capital offers. Parafin’s underwriting engine, for example, operates primarily on sales history within the host platform. You do not need to pull bank statements or accounting records on day one to launch a functioning product.

Once the initial product is live and generating real repayment data, you layer in accounting integrations through QuickBooks or Xero connectors to improve approval rates and increase the average offer size over time. This staged integration approach also carries lower compliance risk. You are not handling sensitive external financial data — with all the disclosure obligations that entails before your compliance posture is fully established.

Think of it as a phased rollout: launch with platform-native data, prove the product works with your merchants, then deepen the underwriting stack as you grow.

4. Surface Pre-Approved Offers Inside Your Merchants’ Natural Workflows

The highest-converting embedded RBF products do not require the merchant to apply for anything. Instead, they display a pre-approved offer already calculated, already approved with a specific amount, a revenue share rate, and a clearly stated repayment cap, at the exact moment in the user’s workflow when capital is most relevant.

This is a fundamentally different experience from sending a marketing email about a financing program. When a merchant sees a capital offer inside the dashboard they check every morning to review yesterday’s sales, the context conversion is entirely different. They are already thinking about revenue. The offer belongs there.

The most effective in-product placement triggers include the main dashboard home screen after a merchant records a strong revenue month, the cash flow or financial reporting module when reviewing business trends, an onboarding milestone notification after ninety days of consistent platform activity, and a seasonal capital prompt timed to known inventory purchasing cycles for retail or hospitality merchants.

The underlying principle is simple but important: meet merchants where they are already thinking about money. In-context placement outperforms any email campaign or standalone application flow by a wide margin in conversion rate.

5. Build the Capital Experience Under Your Own Brand

Merchants should see your platform’s branding at every touchpoint of the capital experience not the name of the infrastructure provider sitting behind it. Most embedded lending APIs fully support white-labeled experiences where offer presentation, acceptance flows, repayment dashboards, and even bank transfer descriptors reflect your product identity.

This matters commercially for a straightforward reason. When a merchant associates working capital access with your platform, that relationship equity belongs to you. It reinforces platform stickiness and makes your product harder to replace. When the merchant thinks of the capital as coming from a third-party lender they happen to access through your app, you lose the relationship benefit entirely while still bearing the integration cost.

The practical configuration for a fully white-labeled experience includes custom offer copy and branded UI components integrated within your existing design system, webhook integrations for offer acceptance events and repayment milestones so your platform stays in sync with loan status, and branded bank transfer descriptors on both disbursement and repayment transactions so the merchant sees your name on every statement line.

6. Configure Repayment Logic That Mirrors Your Platform’s Payment Cycles

Repayment should feel native and predictable to the merchant not like a separate financial obligation running on a foreign schedule. The most effective embedded RBF implementations align repayment cadence directly with how the platform already moves money.

If your platform settles payments to merchants weekly, configure repayment deductions on a weekly basis. If your merchants operate on monthly billing cycles, monthly repayment aligned to their billing rhythm avoids cash flow surprises. Repayment that fits naturally into existing financial patterns sees lower default rates and higher merchant satisfaction scores.

Architect’s Note: The repayment cap is the most important economic variable for the merchant to understand clearly. The total repayment amount equals the principal multiplied by a factor rate, which typically runs between 1.1x and 1.5x for platform-embedded RBF. Factor rates on embedded products are generally lower than standalone MCA products because the platform’s native data provides significantly better risk signals. Lead with that comparison when introducing the product to merchants who are familiar with higher-cost alternatives.

7. Build Underwriting Feedback Loops Using Platform Repayment Data

Once your first cohort of merchants has repaid their initial advances, you possess the most strategically valuable asset in lending: a ground-truth dataset linking repayment outcomes to specific platform behavior signals.

Work with your infrastructure provider to feed that repayment performance data back into the underwriting model on an ongoing basis. Over time, this process creates a platform-specific risk model that outperforms generic industry benchmarks. Merchants on your platform who consistently use certain features, maintain above-average customer retention rates, or exceed specific gross merchandise volume thresholds will correlate measurably with lower default probabilities. Those correlations become proprietary underwriting advantages that external competitors cannot access or replicate.

This feedback loop is precisely how Parafin built its competitive defensibility. Training on repayment data from over two million small businesses across multiple platform environments creates a model that a new market entrant simply cannot build quickly, regardless of how much funding they raise. Data volume is the moat.

The implication for vertical SaaS platforms is direct: the earlier you launch embedded RBF, the earlier the proprietary data accumulation begins, and the wider the underwriting advantage becomes over time.

Follow the Proven Sequence: Payments First, Capital Second, Banking Third

The single most damaging implementation mistake and the one most commonly made is launching embedded payments, lending, and banking products simultaneously in one large release. Each financial product layer carries genuinely different compliance requirements, operational infrastructure needs, and economic complexity. Treating them as one project compounds the risk of all three at once.

The sequence that consistently works across vertical SaaS is straightforward.

Start with embedded payments. Build transaction history, establish your compliance posture with payment processors and regulators, and develop a deep understanding of your merchants’ cash flow patterns before you introduce credit products.

Add embedded RBF second. Once you have ninety or more days of payment data per merchant and a stable operational foundation, surface pre-approved capital offers to qualifying merchants. The underwriting signal is there. The compliance groundwork is in place. The merchant already trusts the platform.

Common Mistakes to Avoid When Embedding RBF in SMB Software

Launching before you have enough merchant tenure data. A merchant with thirty days of platform history produces almost no reliable predictive signal for underwriting. Set a clear minimum threshold typically ninety to one hundred and eighty days of platform history or ten thousand dollars or more in processed volume before any capital offers are surfaced. Launching too early produces low-quality approvals, higher defaults, and damages the product’s reputation with early users.

Treating compliance as a later-stage problem. CFPB Section 1033 open banking rules, state-level lending license requirements, and KYB and AML obligations vary by jurisdiction and product type. Your infrastructure provider handles the lending compliance layer. However, you remain responsible for how customer financial data flows through your system, what disclosures appear during the offer acceptance flow, and how data sharing is documented in your terms of service. Do this before go-live, not after.

Skipping the merchant education layer. Despite growing awareness, many SMB owners still conflate revenue-based financing with high-interest merchant cash advances and approach it with suspicion. A brief, plain-language in-product explanation of how repayment works, what the total cost of capital is in dollar terms, and how it specifically differs from a bank loan significantly increases offer acceptance rates. This does not need to be long three to five clear sentences at the offer screen level is sufficient.

Underestimating the integration timeline. A baseline embedded capital integration with a provider like Parafin or Kanmon typically requires four to eight weeks in a sandbox environment, followed by two to four additional weeks for compliance review, legal contract finalization, and production go-live approval. Budget six to twelve weeks total from kickoff to the first live merchant offer. Promising a faster timeline to internal stakeholders without accounting for that review period creates unnecessary pressure and often results in compliance corners being cut.

Frequently Asked Questions

What is revenue-based financing in SMB software?

Revenue-based financing embedded in SMB software is a capital product where a vertical SaaS platform or marketplace surfaces pre-approved working capital offers directly to its small business customers. Funding is provided through a third-party infrastructure provider, and repayment is automatically deducted as a percentage of the merchant’s ongoing revenue. The SMB receives capital without filling out a traditional loan application, and the platform earns a revenue share fee on funded volume.

How do SMB software platforms offer embedded lending without holding credit risk?

Platforms partner with embedded lending infrastructure providers such as Parafin, Kanmon, or Liberis. Those providers handle origination, underwriting decisions, loan servicing, and in most cases the balance sheet risk as well. The platform contributes data access and the customer-facing product surface. In exchange, it earns referral fees or revenue-share compensation with no direct credit exposure on its books.

What data does an embedded RBF provider use to underwrite SMBs?

The most accurate underwriting models layer three data sources together: banking transaction history accessed via open banking APIs like Plaid or CFPB 1033-compliant feeds, accounting records pulled through QuickBooks or Xero integrations, and native commerce and platform activity data the host platform already collects. Platforms with all three layers integrated approve financing in hours. Platforms relying on manual document uploads take weeks.

What is the difference between revenue-based financing and a merchant cash advance?

Both products deliver upfront capital repaid as a percentage of future revenue. The key differences are in repayment mechanics and cost. MCAs typically use daily deductions tied to card batch processing, carry higher factor rates between 1.2x and 1.5x or more, and have shorter repayment windows with less predictability. RBF uses monthly repayment cadences, offers lower factor rates when backed by richer platform data, and defines a clear total repayment cap so the merchant always knows the maximum they will pay.

How long does it take to integrate an embedded lending API into an SMB software platform?

A baseline integration with providers like Parafin or Kanmon takes four to eight weeks in a sandbox environment plus two to four weeks for compliance review and production go-live, totaling six to twelve weeks from kickoff to the first live merchant offer. Platforms that already have embedded payments infrastructure and clean transaction data pipelines typically land at the shorter end of that range.

Is revenue-based financing right for all SMB software platforms?

Embedded RBF works best for vertical SaaS platforms that already process payments for their SMB customers, have at least ninety days of transaction history per merchant, and serve businesses with at least ten thousand dollars in monthly gross volume. Platforms without payment processing relationships or with very thin transaction histories will need to build the data foundation first before an embedded lending product will generate meaningful approval rates.

Conclusion

Embedding revenue-based financing in SMB software is no longer an exclusive capability of Shopify or DoorDash-scale platforms. The infrastructure layer Parafin, Kanmon, Pipe, Liberis, and others has matured to the point where a Series A vertical SaaS company can integrate a fully white-labeled working capital product in a single quarter without holding credit risk, building compliance infrastructure, or hiring a lending team.

However, the difference between platforms that build a compounding revenue and retention driver and those that see low adoption comes down to three fundamentals. First, the depth of the underwriting data layer how many live signals you can feed into the engine. Second, the placement quality whether offers appear where merchants are already thinking about money. Third, the rollout sequence payments before capital, capital before banking, with each layer compounding on the last.

Get those three right and embedded RBF stops being a product feature and starts being a structural part of your platform’s unit economics.

Explore more guides on vertical SaaS monetization, fintech infrastructure, and AI-powered financial workflows at agentiveaiagents.com.