The Best Way to Handle Fixed Assets in Accounting Software: A Step-by-Step Controller’s Guide

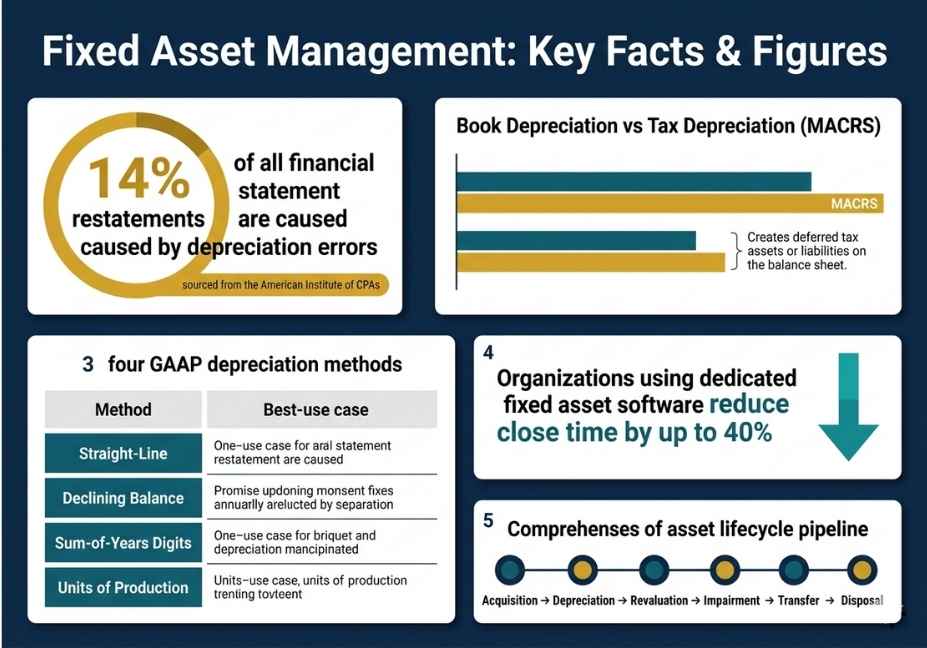

While invoice processing may cause sleepless nights for many finance departments, it is the fixed assets that do. A single missed in-service date; a single ghost asset remaining on the register; and a single depreciation method incorrectly applied to the wrong asset class can severely distort the accuracy of each of the financial statements produced by a company. According to the AICPA, depreciation-related errors lead to an estimated 14% of all financial statement restatements. That’s a staggering number, particularly when you consider nearly all of these errors could have been avoided.

The proper way to manage fixed assets in an accounting software package is not simply to enter a purchase and hit the save button. Rather, it is a structured, policy-driven process that commences with the approval of a capital expenditure and ends with the disposal and removal of an asset from the accounting register. This guide provides detailed, step-by-step descriptions of these processes to provide controllers and finance managers with the necessary information they work with every day – instead of a product review from varying vendors, but from a practitioner’s point of view.

What Is a Fixed Asset in Accounting? A Clear Definition

A fixed asset is a long-lived tangible asset that a business owns and uses to generate revenue, rather than selling it in the ordinary course of operations. Property, plant and equipment commonly abbreviated as PP&E is the formal accounting term for this category. Examples include machinery, buildings, vehicles, computers, and manufacturing equipment.

What makes fixed assets distinct from other costs is that their value is not expensed immediately. Instead, their cost is spread over their useful economic life through depreciation, which is the systematic allocation of an asset’s cost to the periods that benefit from its use. This is a fundamental principle of accrual accounting: match expenses to the revenue they help generate. Because of this, the way a business records and manages its fixed asset register has a direct and lasting impact on the income statement, the balance sheet, and tax filings simultaneously.

Why Does Accounting Software Change the Game for Fixed Asset Management?

Before dedicated software, most organisations tracked fixed assets in spreadsheets. That approach breaks down quickly for three compounding reasons. First, depreciation calculations multiply across hundreds of assets at once, making manual accuracy nearly impossible to sustain. Second, audit trails disappear the moment someone edits a cell without logging the change. Third, ghost assets accumulate items that no longer exist physically but remain on the books quietly inflating depreciation expense and insurance premiums year after year.

Dedicated fixed asset accounting software solves all three problems, but only when it is configured correctly from the start. The software itself is not the solution. The process, the policy, and the discipline behind the software are what determine whether the asset register is trustworthy or not.

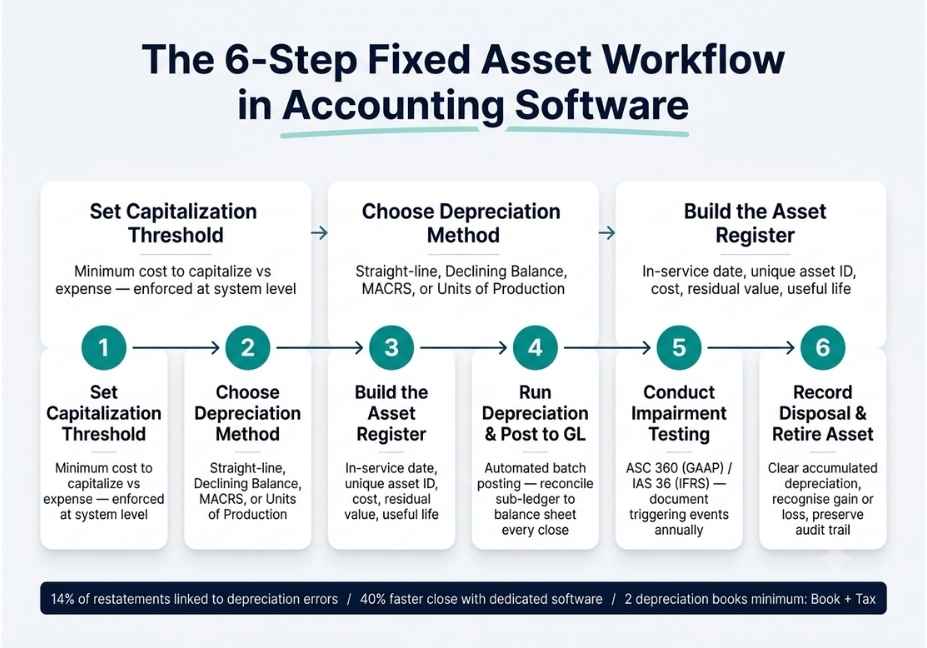

Step 1: Set a Capitalization Threshold This Is Where Everything Starts

The single most important configuration decision in fixed asset accounting is establishing a clear capitalisation threshold before a single asset record is created. A capitalisation threshold is the minimum cost at which a purchase is recorded as a fixed asset on the balance sheet rather than expensed immediately in the current period.

Why does this matter so much? Because without it, different departments make different judgement calls. One manager capitalises a $600 printer. Another expenses a $3,000 server upgrade. The result is an asset register that is inconsistent by design, difficult to audit, and unreliable as a basis for financial reporting.

For most small businesses, a threshold of $1,000 to $2,500 is common. For mid-market and enterprise organisations, $5,000 to $10,000 is typical. Whichever figure you choose, it must be documented formally in your accounting policy, applied consistently across every department and location, and configured directly in your software as a system-level rule rather than left to individual discretion.

A useful calibration point for US businesses: the IRS de minimis safe harbour allows businesses without an applicable financial statement to expense items costing $2,500 or less per invoice or item. Setting your capitalisation threshold at or just above this level naturally aligns your book and tax treatment for smaller purchases, reducing the number of assets that require dual-track accounting.

Step 2: Choose the Right Depreciation Method And Understand Why It Matters

Choosing a depreciation method is the most consequential setup decision in the entire fixed asset workflow. Therefore, it deserves more attention than most guides give it. The method you choose determines how quickly an asset’s cost flows through the income statement, how the asset’s carrying value appears on the balance sheet, and how the depreciation schedule interacts with your tax obligations.

The declining balance method, most commonly applied at 200% (also called double-declining balance), front-loads depreciation expense. Because it charges a higher percentage in the early years and a lower one later, it is a better fit for technology assets and vehicles that lose value most rapidly soon after acquisition. This method reflects the economic reality of fast-depreciating assets more accurately than straight-line does.

For US tax reporting, however, most tangible assets must be depreciated using MACRS the Modified Accelerated Cost Recovery System. IRS Publication 946 defines the MACRS recovery classes, which range from three-year property such as certain farm tools all the way to 39-year non-residential real property. Critically, MACRS produces a different annual depreciation expense than straight-line book depreciation. This difference creates temporary timing differences that appear on the balance sheet as deferred tax assets or liabilities. For this reason, running a single depreciation book is not viable for any business that files a US tax return. Maintaining separate book and tax depreciation records is the minimum viable configuration.

For organisations reporting under IFRS, the IAS 16 standard for property, plant and equipment requires annual review of useful lives, residual values, and depreciation methods. Moreover, IAS 16 mandates component depreciation when an asset’s parts have materially different useful lives. A commercial building, for instance, must have separate depreciation schedules for the structure, the roof, the HVAC system, and the elevators. This level of granularity is not required under US GAAP, where component depreciation is permitted but rarely used an important distinction when configuring software for multi-jurisdiction reporting.

Step 3: Build a Complete Asset Register at Acquisition

Every asset added to the system should carry a consistent and complete set of fields at the moment of creation. Missing data at acquisition does not stay isolated it compounds over the asset’s entire service life and becomes genuinely painful during disposal or audit.

At a minimum, each asset record must include a unique asset ID that can be linked to a physical barcode or QR code for field verification. It should also capture the acquisition date and total purchase price, including installation and transportation costs, because both form part of the asset’s capitalisable cost under GAAP ASC 360 and IFRS IAS 16. Beyond that, the record needs the vendor reference or purchase order number, the asset class and assigned cost centre, the selected depreciation method and estimated useful life, the expected residual value at the end of that useful life, and most importantly the in-service date.

That last field deserves special attention, because it is one of the most consistently mishandled elements in fixed asset setup. Under both GAAP and IFRS, depreciation begins when an asset is ready for its intended use not when it is purchased, not when it is delivered, and not when the invoice is paid. Configuring your software to use the in-service date rather than the invoice date prevents premature depreciation expense recognition, which is a frequent and easily avoidable audit finding.

Step 4: Run Depreciation and Reconcile to the General Ledger Every Period

This is where purpose-built fixed asset accounting software earns its value. Best-in-class platforms run depreciation as a batch process across the entire register and post the resulting journal entries automatically to the general ledger. As a result, the manual effort and transcription risk that come with month-end close are significantly reduced. According to CPCON Group’s analysis of finance teams that migrated from spreadsheet-based tracking, organisations implementing dedicated fixed asset software reduce close time for fixed asset reporting by up to 40%.

What matters in the monthly depreciation run, however, is verification not just execution. Confirm that the depreciation period aligns with your fiscal calendar. Check for assets placed in service mid-month to ensure pro-rata calculations have been applied correctly. Verify that fully depreciated assets have stopped accumulating expense, because continuing to depreciate a fully depreciated asset artificially inflates costs. Finally, reconcile the total accumulated depreciation balance in the asset sub-ledger against the accumulated depreciation account on the balance sheet. If those two figures do not match, you either have an unposted depreciation run or a manual journal entry in the GL that has no corresponding record in the asset sub-ledger.

Building a standing reconciliation report that runs at every close cycle is one of the highest-return configuration investments you can make in your fixed asset software.

CapEx vs OpEx: How Capitalisation Decisions Affect Your Asset Register

One of the most important and most frequently contested decisions in fixed asset accounting is whether a given expenditure should be capitalised as a fixed asset or expensed immediately as an operating cost. This is the CapEx versus OpEx distinction, and it has a direct impact on both the balance sheet and the income statement.

As a general rule, an expenditure is capitalised when it extends the useful life of an asset, significantly improves its performance, or adds new capability. Routine maintenance and repairs, by contrast, are expensed in the period they occur because they simply restore the asset to its expected operating condition rather than enhancing it.

In practice, the line between a capital improvement and a repair is not always obvious. This is precisely why your capitalisation policy and the threshold that enforces it must be documented and applied consistently. Inconsistent CapEx versus OpEx treatment is one of the most common audit findings in fixed asset reviews, and it is also one of the clearest signals to auditors that a finance team lacks internal controls around asset management.

What Is Net Book Value, and Why Does It Drive Disposal Accounting?

Net book value often abbreviated as NBV is the carrying value of a fixed asset on the balance sheet at any given point in time. It is calculated as the asset’s original cost minus accumulated depreciation to date. As depreciation is charged each period, the net book value declines, eventually reaching the asset’s estimated residual value at the end of its useful life.

Understanding net book value matters because it is the figure that determines the gain or loss on disposal. When an asset is sold, scrapped, or written off, the difference between the proceeds received and the net book value at the date of disposal is recognised in the income statement as either a gain or a loss on disposal. If the asset is sold for more than its net book value, a gain is recognised. If it is sold for less or simply scrapped with no proceeds a loss is recorded.

This calculation must be driven by the software, not done manually, because even a one-day error in the disposal date changes the accumulated depreciation balance and therefore the net book value at disposal.

Step 5: Test for Impairment Before Auditors Ask About It

Impairment is one of the most consistently skipped steps in fixed asset management and it tends to surface as an audit finding rather than a proactive finance decision. ASC 360 governs the impairment and disposal of long-lived assets under GAAP; IAS 36 governs it under IFRS. Both standards require an assessment of whether an asset’s carrying value exceeds its recoverable amount when triggering events occur.

Common triggering events include a significant decline in market value, physical damage or technological obsolescence, adverse regulatory changes that affect how the asset can be used, and any plan to dispose of the asset before the end of its originally estimated useful life. Most accounting software does not automatically detect these events. That awareness must come from the finance team, the operations team, or whoever is closest to the physical asset.

Build an annual impairment review into your close calendar. Document the outcome even when no write-down is required the absence of documentation is itself an audit risk under both ASC 360 and IAS 36. Under IFRS, the annual review extends beyond impairment to include reassessment of useful life and residual value. Under GAAP, changing a depreciation estimate is treated prospectively with documented justification.

Step 6: Record Asset Disposals Precisely and Retire Assets Cleanly

Asset disposal whether through sale, trade-in, scrapping, or write-off generates a gain or loss that flows directly to the income statement. Mishandling disposal accounting is one of the most common sources of fixed asset errors, and it typically traces back to a software workflow that was never properly configured.

The correct disposal process clears accumulated depreciation from the contra account, removes the asset’s original cost from the fixed asset account, recognises any proceeds received, and posts the resulting gain or loss to the income statement. In your accounting software, the disposal or retirement workflow should handle all of these steps together rather than requiring separate manual journals for each component. Furthermore, the asset record must be moved to a historical register rather than deleted the full history of cost, depreciation, method, useful life, and disposal proceeds must be retained for audit purposes and for tax filings.

For US tax depreciation, disposal can trigger depreciation recapture, where the IRS taxes previously claimed MACRS deductions as ordinary income rather than at capital gains rates when the asset is sold for more than its tax book value. This means your tax depreciation book must carry the correct tax basis at the point of disposal not the book basis. This is another reason why a single-book setup is a structural liability rather than a simplification.

The Most Common Fixed Asset Mistakes in Accounting Software and How to Avoid Them

Most fixed asset errors are not failures of technology. They are failures of process and policy that software makes visible. Understanding the most common mistakes is therefore more valuable than knowing the most impressive features in any given platform.

Continuing to depreciate fully depreciated assets is the most straightforward error. Software should stop automatically once accumulated depreciation equals the depreciable base but only if the residual value was entered correctly at the time of asset creation. If the residual value field was left blank or set to zero incorrectly, depreciation may continue beyond the point where the asset is fully written down.

Using the purchase date instead of the in-service date causes depreciation to begin early, which shifts expense into earlier periods and eventually causes the useful life calculation to drift out of alignment with the asset’s actual service period.

Running a single depreciation book, as discussed above, forces manual reconciliation between book and tax values at year-end a process that consumes significant time and introduces transcription errors in proportion to the size of the asset register.

Never running a physical inventory allows ghost assets to accumulate silently across multiple close cycles. A ghost asset remains on the books generating depreciation expense and insurance costs even after the physical asset has been disposed of, lost, or stolen. Annual physical verification and reconciliation against the register is the only reliable way to eliminate ghost assets.

Finally, inconsistent capitalisation treatment across departments where finance approves a policy that operations teams never follow in practice creates mixed treatment across asset classes that auditors identify immediately. The corrective is simple in theory but requires discipline in execution: the policy must be enforced at the point of entry in the software, not reviewed after the fact at close.

FAQ: The Questions Controllers and Finance Managers Ask Most

What is the best way to record a fixed asset purchase in accounting software?

Record the asset at its full acquisition cost, including installation and transportation charges. Assign a unique asset ID, enter the in-service date rather than the invoice date, select a depreciation method that reflects how the asset actually loses value, and configure both a book depreciation record and a tax depreciation record from the start. Depreciation begins on the in-service date under both GAAP and IFRS not when the invoice is paid.

How do you set up a depreciation schedule in accounting software?

Configure each asset with its depreciation method, estimated useful life, and residual value. The software then calculates the depreciation schedule automatically. Run depreciation as a batch process at each period close, verify the output against your GL depreciation accounts, and reconcile accumulated depreciation in the asset sub-ledger to the balance sheet balance. Best-in-class platforms post GL entries without requiring manual journals.

What depreciation method should I use for fixed assets?

It depends on the asset type and your reporting framework. Straight-line is most appropriate for buildings and long-lived assets where benefit is consumed evenly. MACRS is required for US federal tax purposes. Declining balance works best for technology and vehicles that lose value quickly in their early years. Units-of-production is most accurate for manufacturing equipment where wear is driven by usage rather than time.

What is the difference between book depreciation and tax depreciation?

Book depreciation follows GAAP or IFRS and is designed to match the cost of an asset to the revenue it generates over its useful life. Tax depreciation in the US follows MACRS rules and is designed by the IRS to accelerate deductions as an incentive for capital investment. The two calculations produce different annual amounts, creating temporary timing differences that appear on the balance sheet as deferred tax assets or liabilities.

What happens when a fixed asset is fully depreciated?

When accumulated depreciation equals the asset’s depreciable base its original cost minus residual value the asset is considered fully depreciated. At that point, depreciation expense stops entirely. The asset remains on the balance sheet at its residual value until it is disposed of. Continuing to charge depreciation after full depreciation is an accounting error that inflates expenses and distorts the income statement.

How do you write off a fixed asset in accounting software?

Use the software’s dedicated disposal or retirement workflow rather than deleting the record. The write-off process clears accumulated depreciation, removes the original cost from the asset account, and posts any resulting loss on disposal to the income statement. The complete asset record must be retained in the historical register for audit trail and tax filing purposes.

How do you handle fixed asset impairment in accounting software?

Impairment is required when a triggering event physical damage, market decline, or intent to dispose early indicates the asset’s carrying value exceeds its recoverable amount. Document the triggering event, perform the impairment test under ASC 360 (GAAP) or IAS 36 (IFRS), and record any write-down as an impairment loss. Most software requires a manual journal entry for the impairment charge, because the system does not automatically detect triggering events.

Conclusion: Get the Fundamentals Right and the Software Does the Rest

Handling fixed assets correctly in accounting software comes down to three things that compound over time: discipline at the point of acquisition, multi-book depreciation configured from day one, and a disposal workflow that closes the loop cleanly without distorting the general ledger or the tax return.

The software does not create accuracy. The policy behind the software creates accuracy. Therefore, the most important investment any finance team can make is not selecting a more powerful platform it is documenting the rules, enforcing them at the point of entry, and reviewing the results at every close cycle.

When those fundamentals are in place, fixed asset management becomes one of the most reliable and auditable areas of a company’s financial close rather than one of the most stressful. Start with the capitalisation threshold, build the depreciation setup with care, and let the software automate everything that follows.

For more accounting systems deep-dives, financial operations workflows, and practical finance guides, visit agentiveaiagents.com.

2 Comments