PEX Fintech AI vs Automation: What’s Actually Running Your Expense Workflows

A prevalent issue faced by finance departments is the tendency to utilize an “AI-powered” platform which would ideally improve their decision-making capabilities. Assuming that this platform employs advanced decision-making capabilities enables these departments to trust a deterministic rule-based machine for months, while they believe that they have relied on an intelligent system. As reported in the 2022 DataRails CFO Report’s findings, more than seventy-five percent of CFO’s will still be the most manually intense positions at C-Suite-level even after implementing so-called AI technologies.

PEX FinTech AI versus Automation this isn’t merely a marketing topic or type of consideration. This is more an issue of architecture; PEX (Prepaid Expense Cards) is one of the leading spend management platforms available for both Small-to-Medium-sized Business and Business-to-Business financial officers to use for expense account management. However, PEX uses rule-based automated transactions along with actual machine learning in ways that have not be communicated to their users in an effective manner. Therefore finance departments either tend to over trust the AI component or spend too much time completing tasks that should be automatically completed by the automation component.

In this article we will outline where PEX is actually using real ML inferences and where they are using a deterministic rule engine in order to better assist you in building smart workflows around the PEX platform.

What Is the Difference Between AI and Automation in Fintech?

Automation in fintech follows fixed, pre-programmed rules. It performs the same action every time a condition is met, without any learning or adaptation. AI in fintech specifically machine learning analyzes historical data, identifies patterns, and improves its predictions over time without needing manual rule updates.

In short: automation is consistent but rigid. AI is adaptive but requires training data to perform well.

PEX uses both layers inside the same platform. Furthermore, these two layers serve different purposes and operate at different points in the expense management workflow. Understanding which is which directly affects how much you can trust the system and where human review remains essential.

Featured Answer (for Google’s featured snippet): Automation in fintech executes predefined rules the same action every time a condition is met with no learning. AI in fintech uses supervised machine learning models that learn from historical transaction data, improve over time, and handle edge cases that explicit rules cannot anticipate. PEX uses both within its spend management platform.

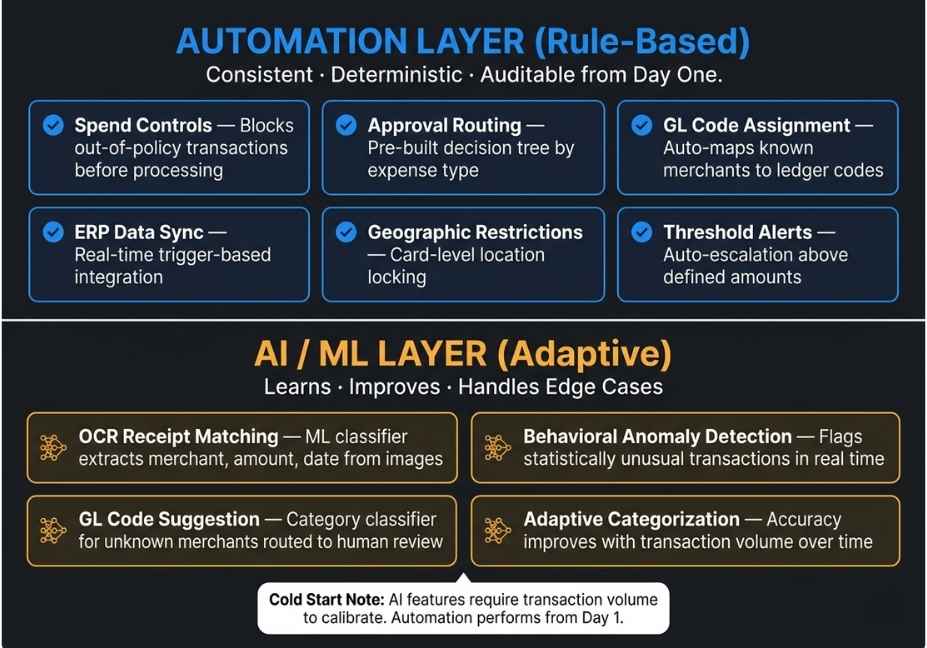

How PEX’s Rule-Based Automation Layer Works

PEX built its automation layer first, and it remains the most reliable part of the platform. These are deterministic workflows therefore, they produce consistent, auditable outputs every single time.

Spend controls are the clearest example of this automation layer at work. Finance administrators pre-configure rules at the card or cardholder level. For instance:

- A field team’s cards work only at approved merchant category codes

- Any transaction above a defined dollar threshold triggers a manager approval request automatically

- Geographic restrictions block purchases outside specific states or regions

Because these controls execute before a transaction processes, they prevent policy violations rather than catching them after the fact. That is a fundamentally different value proposition from AI anomaly detection, which we will cover next.

The approval workflow engine similarly runs on explicit logic. When a cardholder submits an expense, the system routes it to the correct approver based on a pre-built decision tree the VP of Marketing for marketing expenses, for instance, or the department head for operational costs. There is no inference involved. The routing logic is transparent, repeatable, and auditable.

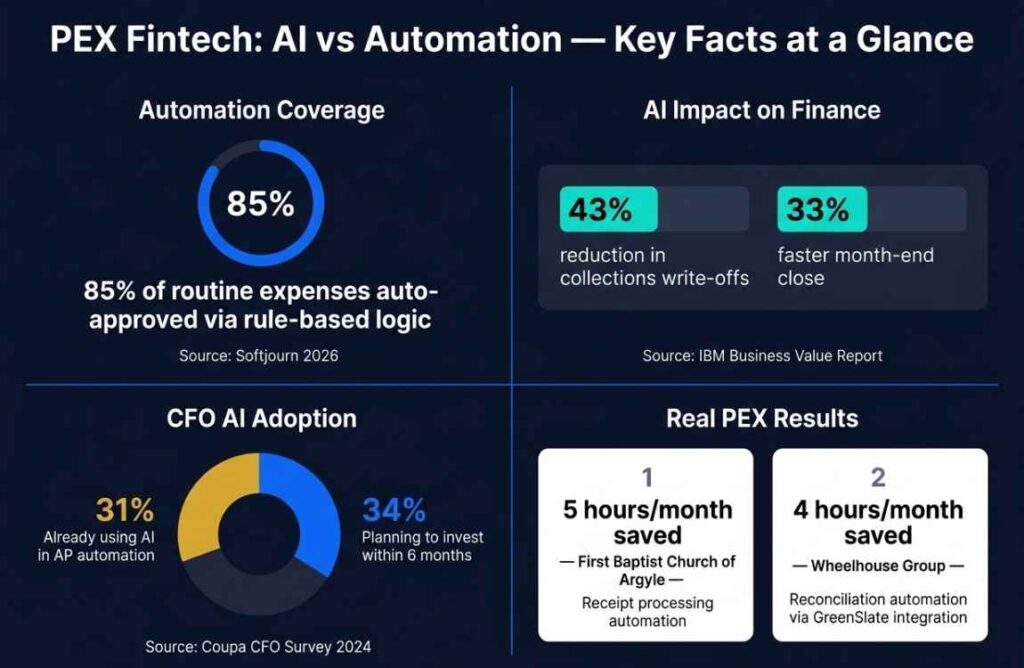

GL code pre-assignment also lives inside this automation layer. Finance teams map merchant names or merchant category codes to General Ledger accounts once during setup. As a result, every subsequent transaction at that merchant auto-populates the correct ledger line without any human input. Softjourn’s 2026 analysis of expense management platforms found that leading systems can automatically approve roughly 85% of routine expenses within policy — and almost all of that comes from rule-based logic, not machine learning.

Pro Tip: Set up your GL mapping and spend controls before you enable any AI features. The automation layer generates clean, consistent transaction data. Consequently, the ML models that run on top of it become significantly more accurate because they train on higher-quality inputs.

Now that you understand how the automation layer works, let’s look at where PEX introduces real machine learning.

Where PEX Uses Real Machine Learning

The AI layer in PEX handles the cases that explicit rules cannot anticipate. In contrast to the automation layer, these features learn from data over time. However, they are task-specific supervised models not generative AI, not large language models, and not autonomous agents.

OCR-Based Receipt Matching

When a cardholder submits a receipt photo, PEX runs it through an Optical Character Recognition pipeline combined with a trained ML classifier. The system extracts three key attributes from the image: merchant name, transaction amount, and date. It then matches those attributes to the corresponding card transaction automatically.

Furthermore, the model generalizes across receipt formats. A handwritten receipt from a hardware store and a digital receipt from an airline look completely different structurally. Nevertheless, the classifier handles both because it has learned from thousands of confirmed matches, not from a hardcoded template. This is a genuine supervised learning loop, and its accuracy improves with transaction volume.

Anomaly Detection for Fraud Prevention

PEX’s fraud detection layer uses behavioral ML models that build spending pattern baselines at the employee, department, and organizational level. When a transaction deviates significantly from that baseline an unusual merchant, an atypical transaction time, or an outlier amount the system flags it in real time for review.

This is meaningfully different from spend controls. Spend controls block transactions that violate explicit rules. Anomaly detection, in contrast, catches transactions that follow the rules but still look statistically suspicious. As a result, it catches a class of fraud that no pre-programmed rule engine can anticipate.

According to the IBM Business Value Report on AI in Finance, organizations that deployed AI-driven financial workflows reduced collections write-offs by 43% and cut month-end close time by 33%. PEX’s anomaly detection operates within this category of adaptive, data-informed financial systems.

Intelligent GL Code Suggestion for Unknown Merchants

For merchants that do not yet have a pre-assigned GL mapping, PEX uses an ML classifier to suggest the most likely GL category. The model bases its suggestion on the merchant’s business category, transaction history across the platform, and semantic similarity to known merchant-to-GL mappings.

Importantly, PEX routes these suggestions to a human reviewer rather than auto-posting them. This human-in-the-loop design reflects the cold-start limitation of the model it performs well on common merchant types but loses confidence on novel inputs. Consequently, the review queue exists to catch the cases where the classifier is most likely to be wrong

Real-World Results: What the Combined Architecture Delivers

Two documented PEX case studies illustrate how the layered system performs in production environments.

First Baptist Church of Argyle saved 5 hours per month on receipt chasing and manual expense processing. That outcome came primarily from the automation layer spend controls, pre-assigned GL codes, and auto-syncing eliminated the repetitive manual steps their team previously handled individually.

Wheelhouse Group saved 4 hours per month on reconciliation through PEX’s integration with accounting partner GreenSlate. In that case, rule-based automation handled the volume workload, while the AI receipt matching layer reduced the exception queue the expenses that would otherwise need manual investigation.

The pattern across both examples is consistent. Automation delivers the volume savings. AI reduces the exception rate. Furthermore, this is the architectural reality of most mature B2B fintech platforms in 2025 and 2026 not end-to-end AI, but a deliberate two-layer system where ML handles precisely the hard cases that deterministic rules cannot address.

Did You Know? The Coupa Strategic CFO Survey 2024 found that 31% of CFOs already use AI in AP automation workflows, with 34% planning to invest within six months. As a result, understanding the AI vs automation distinction has become a practical procurement skill for finance leaders.

Where PEX’s AI Layer Has Real Limits

PEX’s machine learning capabilities are genuinely useful. However, they come with important constraints that practitioners need to understand before building workflows around them.

No natural language querying. PEX does not expose an LLM interface of any kind. Therefore, you cannot ask the platform “show me all marketing spend above budget in Q3″ in plain language. All querying goes through structured filters and report dashboards.

Model opacity. PEX’s anomaly detection and GL suggestion models are black boxes, similarly to most production fintech ML systems. When the system flags a suspicious transaction, it does not explain why. Finance teams get the alert but not the reasoning. That is a meaningful limitation for audit trails and regulatory compliance.

No agentic decision-making. PEX does not implement autonomous agent loops. There is no planner-executor cycle, no tool-use chain, no cross-session memory retrieval. Finance teams evaluating genuinely agentic workflows for instance, LangChain-orchestrated agents with live ERP API access should treat PEX as a structured data source and rule enforcement engine, not as an autonomous financial actor.

Architect’s Note: If your CFO technology stack roadmap includes agentic finance workflows, PEX’s API is a strong integration target. Its transaction data, spend control configurations, and GL mappings serve as high-quality grounding context for an LLM-based planning agent operating above the platform layer.

What Finance Professionals Are Saying About PEX AI vs Automation

On forums like Reddit r/Accounting and r/CFO, practitioners consistently make the same observation: PEX’s automation features work reliably from day one, while the AI features take time to earn trust.

One senior controller noted that the receipt matching accuracy improved significantly after three months of transaction volume, confirming the supervised learning behavior described in PEX’s product documentation. Another CFO at a mid-sized nonprofit observed that the anomaly detection flagged a duplicate vendor payment that their manual review process had missed for two billing cycles.

In contrast, several users noted that the GL suggestion feature frequently misfires on new vendor types, reinforcing the cold-start limitation and the importance of maintaining the human review queue for unconfirmed suggestions.

FAQ People Also Ask

What is the difference between AI and automation in fintech?

Automation in fintech runs fixed, predefined rules that execute the same action every time a condition is met no learning involved. AI in fintech, specifically machine learning, learns from historical transaction data and improves its predictions over time. In PEX, automation handles spend controls and GL mapping for known merchants. AI handles receipt matching, anomaly detection, and GL suggestions for new merchants.

Does PEX use real AI or just rule-based automation?

PEX uses both. Its spend controls, approval routing, GL mapping for known merchants, and ERP data sync all run on deterministic rule-based automation. In contrast, its receipt matching system uses OCR plus a supervised ML classifier, its fraud detection uses a behavioral anomaly model, and its GL suggestion feature for unknown merchants uses a category classifier. These ML features improve with transaction volume over time.

How does PEX detect fraudulent transactions?

PEX uses two complementary mechanisms. First, rule-based spend controls block transactions that violate explicit policies wrong merchant category, wrong geography, or over-limit amount before they process. Second, a behavioral ML anomaly detection model flags transactions that pass policy checks but deviate statistically from established spending patterns. Because of this two-layer approach, PEX catches both policy violations and subtle suspicious behavior.

What GL coding features does PEX offer?

PEX offers two GL coding modes. For merchants with pre-assigned mappings, it applies the correct GL code automatically through rule-based lookup instant and deterministic. For new or unknown merchants, an ML classifier suggests the most likely GL category based on merchant type and historical similarity. These suggestions route to a human reviewer for confirmation rather than auto-posting, which maintains accuracy on edge cases.

Can PEX integrate with accounting software like NetSuite?

Yes. PEX integrates natively with NetSuite, QuickBooks Online, and over 50 additional ERP and accounting platforms. These integrations use automated rule-based data sync triggers that push transaction and expense data to the connected accounting system in real time. As a result, finance teams eliminate manual CSV exports, reduce reconciliation time, and accelerate month-end close.

How does PEX compare to other fintech tools like Brex and Ramp for AI features?

PEX, Brex, and Ramp all blend rule-based automation with task-specific ML. However, PEX differentiates through its prepaid corporate card model and its deep focus on SMB B2B spend control workflows. Brex and Ramp have invested more heavily in LLM-based natural language querying and AI-generated spend insights. Consequently, teams that need conversational financial analysis may find Brex or Ramp more capable on that front, while teams that prioritize granular card-level control and ERP integration depth often prefer PEX.

Conclusion

The pex fintech ai vs automation distinction comes down to this: PEX runs two separate layers, and they solve different problems. The rule-based automation layer handles policy enforcement at scale consistently, immediately, and auditably from day one. The ML layer handles the exceptions that explicit rules cannot anticipate receipt matching edge cases, behavioral anomalies, and GL suggestions for novel vendors.

For finance practitioners, the practical takeaway is straightforward. Trust the automation layer for volume throughput and audit trails. Treat the AI features as accuracy amplifiers that require transaction history to calibrate and human review to catch edge-case errors. Furthermore, do not expect PEX’s native AI to reason over complex financial questions that is a job for an LLM agent operating above the platform.

Explore more hands-on breakdowns of AI in fintech and agentic system design at agentiveaiagents.com.